WASHINGTON — National Taxpayer Advocate Erin M. Collins today released her Fiscal Year 2027 Objectives Report to Congress, highlighting a largely successful 2026 filing season in which the IRS processed nearly 139 million individual tax returns, issued more than 90 million refunds, and successfully implemented extensive tax law changes despite significant operational challenges. The report also identifies areas where taxpayers experienced refund delays and service challenges, including returns suspended during processing for additional review, delays in receiving paper refund checks, and prolonged case resolution times for victims of identity theft, while outlining the Advocate’s priority recommendations as the IRS continues to modernize its technology systems.

“Entering the 2026 filing season, there was considerable uncertainty about the IRS’s ability to successfully manage a convergence of major challenges: implementation of sweeping new tax legislation, significant workforce reductions, and extensive leadership turnover,” Collins writes. “In the end, the IRS performed better than expected in most respects. The vast majority of taxpayers filed their returns successfully and received their refunds without significant delay. [But] taxpayers who required assistance from the IRS often struggled to get it.”

The report credits the IRS’s continued technology transformation efforts as a primary driver of its success. By the end of the filing season, the IRS had processed about 139 million Forms 1040, U.S. Individual Income Tax Return, and about 98% had been submitted electronically. About 65% of those returns resulted in refunds, and about 98% of refunds were delivered by direct deposit. As a result, the significant majority of returns were processed via automation and without issue, allowing most taxpayers to file their returns and receive their refunds without delay. Figure 1 shows key filing season statistics.

[Note: IRS data on “Refunds Issued” and “Refunds Issued by Direct Deposit” is not directly comparable. “Refunds Issued” includes only current-year refunds, while “Refunds Issued by Direct Deposit” includes refunds issued for prior tax years as well.]

Continued improvements in online accounts provided valuable self-service options for taxpayers. The report notes that taxpayers logged into their Individual Online Accounts nearly 121 million times during the filing season, while the IRS expanded account functionality to allow taxpayers to upload documents in response to certain notices, receive refund status notifications, update direct deposit information in some circumstances, and access additional account information. Taxpayers used their online accounts to view tax documents needed to prepare accurate returns, accessing information returns more than 3.7 million times.

Taxpayers also made extensive use of the IRS’s refund-tracking tools. During the filing season, taxpayers checked the status of their refunds through the IRS’s Where’s My Refund? tool about 346 million times, a 9% increase from the prior year. The report says online accounts and refund-tracking tools give taxpayers access to information when they need it and reduce the need to call the IRS or visit a Taxpayer Assistance Center.

“The IRS is often held up as the poster child for antiquated government technology infrastructure, and there is certainly some truth to that characterization. But the IRS has been improving its technology year by year, and as long as it gets the IT right, most taxpayers file their returns and receive their refunds without delay,” the report says.

While most taxpayers did not encounter problems, the report says “aggregate statistics do not tell the whole story.”

“For millions of taxpayers, the filing season was frustrating, confusing, and financially disruptive. Some taxpayers whose returns were frozen by IRS filters waited weeks or months for refunds they depended on to pay rent, buy groceries, or cover medical expenses. Taxpayers calling certain IRS telephone lines often could not reach a live employee despite repeated attempts. Victims of identity theft continued to face unacceptable delays that, in many cases, stretched close to two years. Lower-income and unbanked taxpayers seeking paper refund checks encountered obstacles and delays that left many feeling shut out of a system that should work for everyone,” the report says.

Refund delays. Even during a successful filing season, millions of returns are frozen by IRS processing filters and subjected to review. This filing season, more than 14 million individual income tax returns were suspended during processing. More than one million taxpayers did not receive their refunds within the IRS’s normal processing time, experiencing an average wait of about 5.5 weeks. A significant but unknown number of taxpayers experienced shorter refund delays that fell within normal processing times.

Telephone and correspondence processing challenges. Taxpayers had more difficulty reaching the IRS by phone during the 2026 filing season than during the 2025 filing season. Overall, the IRS received 48.1 million calls, telephone assistors answered 9.9 million calls (21%), and the average time taxpayers spent waiting on hold was 14 minutes, as compared with 50.2 million calls received, 12.4 million calls answered by telephone assistors (25%), and an average wait time of 8 minutes during the prior filing season.

Historically, the IRS has measured its telephone performance based solely on calls to its Accounts Management telephone lines, and it has used a “Level of Service” measure that excludes calls to other telephone lines, calls routed for automated responses, and calls in which the taxpayer hangs up before being placed in a calling queue. This year, the IRS provided a 73% Level of Service on the Accounts Management lines, and wait times on those lines averaged 8 minutes.

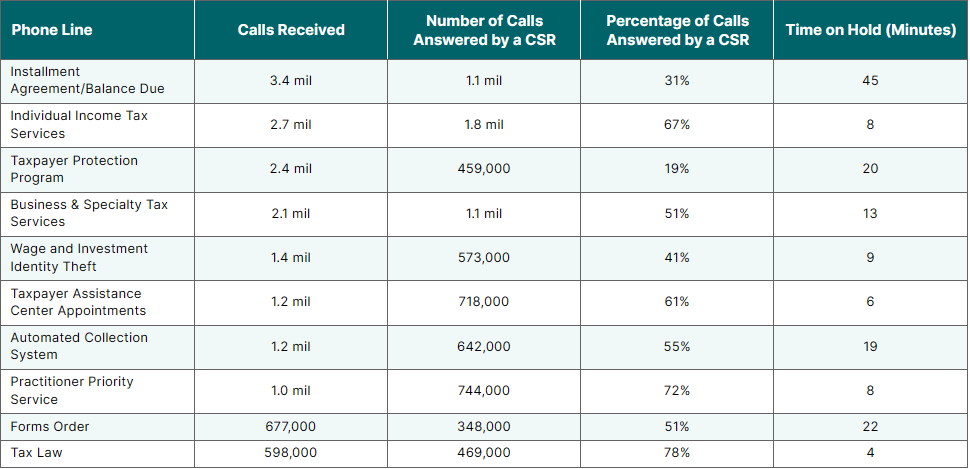

But two of the three highest volume telephone lines do not fall under the Accounts Management umbrella, and taxpayers calling those lines encountered considerable difficulty getting help. About 3.4 million calls were received on the Installment Agreement/Balance Due line, which taxpayers call when they cannot fully pay their tax liabilities and want to set up installment agreements or make other payment arrangements. The IRS only answered 31% of those calls, and taxpayers waited an average of 45 minutes for a telephone assistor to answer. In addition, about 2.4 million calls were received on the Taxpayer Protection Program line, which taxpayers call when their returns are suspended during processing due to suspected identity theft and they need to authenticate their identities to secure the release of their refunds. The IRS only answered 19% of these calls, and taxpayers waited an average of 20 minutes to get through.

The following table shows IRS performance on the 10 telephone lines that received the highest call volumes.

The report points out that employees in the Accounts Management function perform two key roles: (1) they answer telephone calls and (2) they process taxpayer correspondence and work paper-inventory cases. In past years, the IRS established high Level of Service targets, which meant heavily staffing the phones, leading to over a million hours of annual “idle time,” where employees were simply waiting for the phone to ring, and resulting in backlogs of paper inventories. To allocate more resources to paper processing, Collins and others recommended the IRS modestly reduce the Level of Service targets on its Accounts Management lines. The IRS did so, and the report says that decision “produced benefits for many taxpayers whose correspondence and account issues might otherwise have remained unresolved for extended periods.” The impact of the decision on the Accounts Management telephone lines was modest; the lowest performing telephone lines were not Accounts Management lines.

Difficulties obtaining refunds by paper check. During the 2026 filing season, the IRS implemented Executive Order 14247, which generally directs federal agencies to transition toward electronic payments to improve security, reduce fraud risks, and lower administrative costs. Overall, more taxpayers received their refunds by direct deposit this year. But some taxpayers cannot receive their refunds by direct deposit, including unbanked and underbanked taxpayers, lower-income taxpayers, certain elderly taxpayers, taxpayers residing overseas, and other taxpayers for whom electronic payment was not practical or accessible. The EO expressly authorized the Secretary “to revise procedures for granting limited exceptions where electronic payment and collection methods are not feasible,” but the report says the IRS did not establish clear and workable procedures for millions of affected taxpayers, creating confusion, additional work for taxpayers and the IRS alike, and refund delays of 6 weeks or more.

As of April 27, the IRS had issued about 4 million notices for returns that either did not include valid direct deposit information or contained incorrect information. The notices instructed taxpayers to log onto their online accounts to provide or correct their direct deposit information, or to request a waiver to receive a paper check. However, most taxpayers do not have online accounts, and some could not establish them. Even for taxpayers who did have online accounts, the notice omitted critical information that taxpayers needed to make a waiver request. Alternatively, the IRS allowed taxpayers to call the IRS’s 1040 telephone line to request a waiver, but it did not mention that option in its notice.

Continuing delays of about 20 months to resolve identity theft victim assistance cases. For the last 3 years, TAS has reported on “unconscionable” IRS delays in resolving identity theft cases, which often require taxpayers to wait nearly 2 years to receive their refunds. At the end of the filing season, more than half a million cases were pending in inventory. “For many low- and middle-income taxpayers, waiting nearly two years for a refund is not merely an inconvenience [but a financial hardship],” the report says. “For all taxpayers, this delay is frustrating, burdensome, difficult to navigate, and time-consuming.”

Lessons from the filing season. In the report’s preface, Collins says the 2026 filing season highlights a growing divide in tax administration between taxpayers whose issues can be resolved through automated systems and taxpayers whose situations need individualized assistance, manual review, or flexibility. “Taxpayers who fall outside standard processing channels are often the taxpayers who most need assistance, [often] because they are elderly, disabled, limited-English proficient, unbanked, or lacking reliable internet access,” she writes. She adds:

“[A] digital-first strategy can improve tax administration but must not become a digital-only strategy. As the IRS continues to transform its operations, it must preserve meaningful access to telephone assistance, in-person service, clear notices, timely correspondence, and effective case resolution functions. Taxpayers must be able to understand what is expected of them, obtain help when they need it, and trust they will be treated fairly when problems arise. Those principles are fundamental to taxpayer rights and essential to maintaining public confidence in our tax system.”

The report identifies TAS’s key advocacy objectives for the upcoming fiscal year, as the law requires. The report sets out 11 such objectives:

The National Taxpayer Advocate is required by law to submit a year-end report to Congress that, among other things, makes administrative recommendations to resolve taxpayer problems. Internal Revenue Code § 7803(c)(3) authorizes the National Taxpayer Advocate to submit the administrative recommendations to the Commissioner and requires the IRS to respond within 3 months.

The National Taxpayer Advocate made 64 administrative recommendations in her 2025 year-end report and then submitted them for response. The IRS has agreed to implement 47 (or 73%) of the recommendations in full or in part.

Read the IRS responses in the 2025 Annual Report to Congress Report Card.

TAS is an independent organization within the IRS that helps taxpayers resolve problems with the IRS, makes administrative and legislative recommendations to prevent or correct problems and protects taxpayer rights.

The National Taxpayer Advocate is required by statute to submit two annual reports to the House Committee on Ways and Means and the Senate Committee on Finance. The statute requires that the reports be submitted directly to the Committees without any prior review or comment from the Commissioner of Internal Revenue, the Secretary of the Treasury, the IRS Oversight Board, any other officer or employee of the Department of the Treasury or the Office of Management and Budget. The first report must identify the objectives of the Office of the Taxpayer Advocate for the fiscal year beginning in that calendar year. The second report must include a discussion of the 10 most serious problems encountered by taxpayers, identify the 10 tax issues most frequently litigated in the courts, and make administrative and legislative recommendations to resolve taxpayer problems.

Learn more at TaxpayerAdvocate.irs.gov or call 877-777-4778. Get updates on tax topics by following TAS on social media at: facebook.com/YourVoiceAtIRS, instagram.com/yourvoiceatirs, X.com/YourVoiceatIRS, LinkedIn.com/company/taxpayer-advocate-service, and YouTube.com/TASNTA.

Subscribe to receive the National Taxpayer Advocate’s blogs about key issues in tax administration in your inbox or visit the TAS website to read her previous blogs.

For media inquiries, please contact TAS Media Relations at TAS.media@irs.gov or call the TAS media line at (202) 317-6802.

Want to get the latest tax news, learn more about taxpayer rights, and upcoming TAS events while looking at cute dogs and pop culture references? Look no further than TAS Social Media. Follow, like and share our content to help spread the work on how we advocate for taxpayers!