In a series of earlier blogs, I discussed some of the problematic aspects of the international information return (IIR) penalty regime. In Part 1, I advocated that, especially after the Tax Court’s decision in Farhy v. Commissioner, Congress should make Chapter 61 IIR penalties subject to deficiency procedures. In Part 2, I urged Congress to ensure that the statute of limitations in IRC § 6501(c)(8) governs these IIR penalties, while in Part 3, I reiterated my longtime recommendation that “willfulness” be proven by clear and convincing evidence. In this blog, I will address the broad scope of the IIR penalty regime.

There is a misconception that IIR penalties affect primarily bad-faith, wealthy taxpayers who are experiencing consequences of their own making. Reality, however, is much different. The IIR penalty regime disproportionately affects individuals and businesses of more moderate resources, and is by no means just a rich person’s problem. Wealthy individuals and large businesses tend to have knowledgeable and well-informed representation and as a result have fewer foot faults. Immigrants, small businesses, and low-income individuals may not be as well-informed about IIR penalties and may not have return preparers with the same technical expertise on international penalties.

This phenomenon can be seen in the context of IRC §§ 6038 and 6038A penalties, which relate to information reporting of U.S. persons with certain interests in foreign partnerships and corporations, and 25 percent foreign-owned U.S. corporations. These penalties negatively impact several groups, including our immigrant population. If immigrants who are U.S. residents create U.S. business entities and include their family members living abroad, it potentially triggers a filing obligation and has resulted in penalties for failure to timely file an IIR. TAS is also aware of penalties asserted against U.S. persons required to report various items of information concerning dormant foreign corporations, where the taxpayer intended to do business abroad but the business did not undertake transactions. We have also heard about a U.S. citizen who lived overseas and rented out properties located abroad. The citizen was advised to move the properties into a foreign corporation for liability purposes but was unaware of the need to file a Form 5471, Information Return of U.S. Persons With Respect To Certain Foreign Corporations. All of these scenarios can trigger the IIR penalty. When taxpayers voluntarily correct their failures to file, this good-faith action can sometimes have the unexpected effect of causing the IRS to automatically assess the penalty. If the IRS does not administratively abate the penalty, taxpayers will need to pay the penalty in full before challenging the penalty by filing a suit for refund in the United States District Court or the United States Court of Federal Claims.

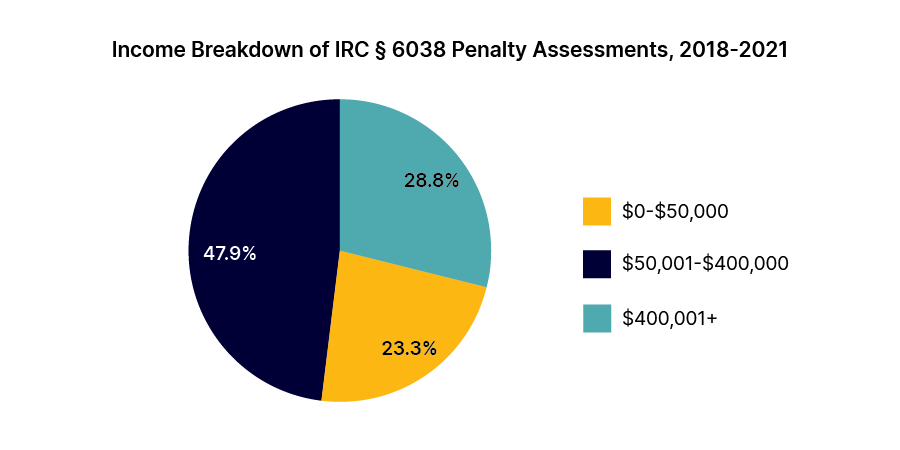

When these penalties are applied to individuals (Individual Master File taxpayers), 71 percent are assessed against taxpayers with income of $400,000 or less. The average penalty amount for these individuals is over $40,000. These results are shown in the following figure:

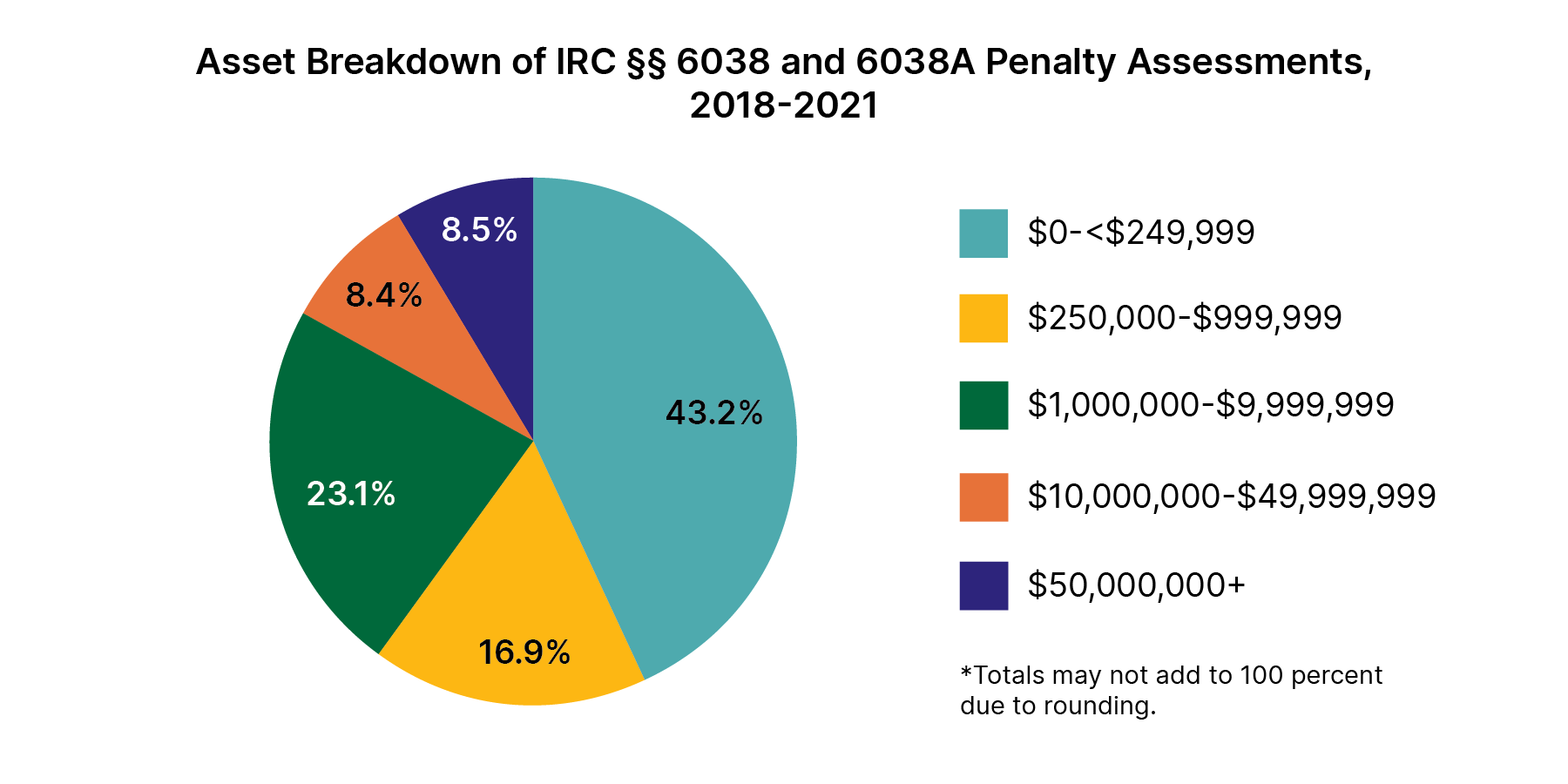

As with lower- and middle-income individuals, small and midsize businesses (Business Master File taxpayers) are heavily impacted by the IIR penalty regime. Among other things, they comprise the overwhelming majority (83 percent) of IRC §§ 6038 and 6038A penalty assessments against businesses, with the remaining 17 percent attributed to large businesses with assets greater than or equal to $10 million. In dollar terms, small and midsize businesses are subject to 64 percent of the aggregate business penalties imposed under IRC §§ 6038 and 6038A. This distribution can be seen in the following figure:

IRC §§ 6038 and 6038A do make provision for abatements for reasonable cause and sometimes taxpayers can receive the first time abatement (FTA) for these penalties if the underlying return receives FTA in the first instance. Nevertheless, even here, better outcomes correlate to greater resources. Analysis undertaken by TAS Research indicates that larger businesses are more likely to receive abatements of IRC § 6038 penalties. Again, my assumption is large businesses have representatives familiar with international tax law and the reasonable cause defense.

The disproportionate nature of IIR penalties is particularly apparent when viewed in the context of IRC § 6039F penalties relating to foreign gift and inheritance reporting. This penalty is imposed against U.S. persons who receive gifts from foreign persons (including trusts and other entities) and fail to file a Form 3520, Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts, in any year in which those gifts meet the dollar threshold. Noncompliance with this filing requirement can be devastating, as the penalties involved can reach up to 25 percent of the value of the gift. When a gift is received from a foreign person there may be no U.S. tax implication. In other words, the recipient can be penalized even though there is no tax due – no underreported income.

TAS is aware of situations in which a foreign grandparent provided a gift to cover the cost of a U.S. grandchild’s living expenses while attending college. In this example, if the amount exceeded the $100,000 threshold, the grandchild has a filing obligation and could be penalized for up to 25 percent even though no U.S. tax liabilities may result from the gift. Similarly, if a U.S. person receives an inheritance from a foreign individual, the recipient is penalized if they do not file a Form 3520, even though the foreign individual may never have had a U.S. filing obligation or tax due.

The available data shows that the IRC § 6039F penalty can be severe. Between 2018 and 2021, there were over 3,700 penalties assessed against individual taxpayers, totaling $844 million. During this period, the average penalty was $226,000. This information is shown by year in the following figure:

| Year | Total penalties assessed | Total dollars assessed | Average penalty (mean) | Median penalty |

|---|---|---|---|---|

| 2018 | 586 | $77,274,037 | $131,867 | $39,160 |

| 2019 | 1,015 | $238,326,771 | $234,805 | $56,560 |

| 2020 | 837 | $282,289,168 | $337,263 | $60,000 |

| 2021 | 1,297 | $246,414,866 | $189,988 | $52,978 |

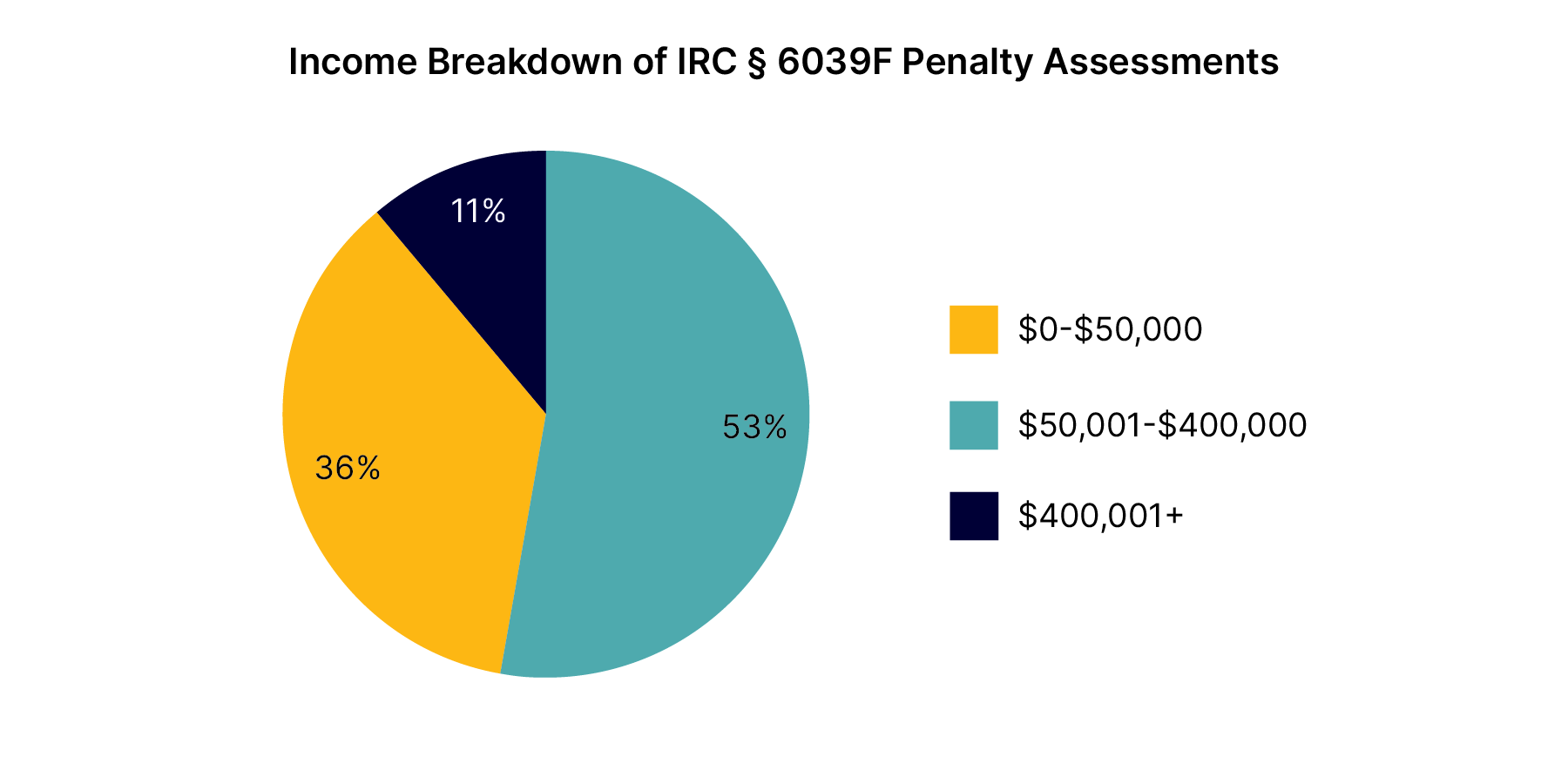

The IRC § 6039F penalties have an especially heavy impact on individual taxpayers: 92 percent were assessed against individuals. Additionally, a startling number of these penalties against individuals – 89 percent – are assessed against lower- and middle-income taxpayers. The following figure illustrates the income breakdown of these assessments:

The penalties assessed against the lower- and middle-income individuals are quite daunting, as well. During the years 2018-2021, the average penalty for taxpayers with $50,000 or less in total positive income was $226,000, while for taxpayers with income ranging between $50,000 and $400,000 in income, the average penalty was $241,000. These penalty levels far exceed what is needed to promote tax compliance and are needlessly punitive.

The fact that these penalties, which are systemically assessed, are abated at rates often exceeding 50 percent highlights the stress and burden this regime places on taxpayers. Taxpayers should not be receiving startling letters informing them of $200,000 penalties that are more likely to be abated than collected. This problem is exacerbated by the circumstance that penalties in this area are not directly eligible for FTA, and that once learning that these penalties have been assessed, taxpayers’ primary administrative remedy is to seek reasonable cause relief, which is purely discretionary on the part of the IRS.

The reach of the IIR penalty regime goes well beyond the mega-wealthy and the Fortune 500. It broadly affects lower- to middle-income individuals and small and midsize businesses. The often-large penalties generated by the regime, combined with other compounding factors, such as the use of systemic assessments and the lack of deficiency procedures, raise serious concerns regarding equity, due process, and access to justice.

Since 2020, I have recommended that the IRS stop automatically assessing IIR penalties and provide taxpayers due process by affording them the opportunity to administratively present their reasonable cause defense and request FTA and consideration by the Independent Office of Appeals prior to any assessments. I also recommend that the IRS expand its administrative relief in the form of FTA to all IIR penalties, including IRC § 6039F penalties, which are imposed when Forms 3520 are not filed. I have advocated for legislation that would subject all IIR penalties to deficiency procedures to provide taxpayers due process and the ability to have the issue heard by the U.S. Tax Court prior to paying the penalty. (See our 2023 and 2022 recommendations in the NTA’s Purple Book of Legislative Recommendations submitted to Congress.) This legislative change would protect the IRS from the future ramifications of the Farhy decision. More importantly, it would provide taxpayers with a more efficient and equitable regime governing the initial imposition of IIR penalties and the mechanisms by which they can be challenged by taxpayers while also protecting their rights.

The views expressed in this blog are solely those of the National Taxpayer Advocate. The National Taxpayer Advocate presents an independent taxpayer perspective that does not necessarily reflect the position of the IRS, the Treasury Department, or the Office of Management and Budget. NTA Blog posts are generally not updated after publication. Posts are accurate as of the original publication date. Portions of this blog may have been developed with the assistance of artificial intelligence. All AI-assisted content has been reviewed, verified, and approved by the National Taxpayer Advocate or TAS staff to ensure accuracy and integrity.